The Black–Scholes Equation

Application ID: 82

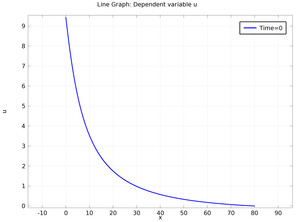

The Black-Scholes equation, computes the value u of a European stock option. Black-Scholes derived an analytical expression for the solution to this problem. However, the formula works only for certain cases; for instance, you cannot employ it when sigma and r are functions of x and t. Here, sigma denotes the volatility, r the continuous compounding rate of interest, and x the underlying asset price.

Using a PDE formulation allows you to determine the price for such cases. This model sets up the PDE formulation of the Black Scholes equation and in addition, this model also shows how to solve the 1D time-dependent variation using a 2D geometry with the y-coordinate corresponding to time.

この model の例は, 通常次の製品を使用して構築されるこのタイプのアプリケーションを示しています.

ただし, これを完全に定義およびモデル化するには, 追加の製品が必要になる場合があります. さらに, この例は, 次の製品の組み合わせのコンポーネントを使用して定義およびモデル化することもできます.

アプリケーションのモデリングに必要な COMSOL® 製品の組み合わせは, 境界条件, 材料特性, フィジックスインターフェース, パーツライブラリなど, いくつかの要因によって異なります. 特定の機能が複数の製品に共通している場合もあります. お客様のモデリングニーズに適した製品の組み合わせを決定するために, 製品仕様一覧 を確認し, 無償のトライアルライセンスをご利用ください. COMSOL セールスおよびサポートチームでは, この件に関するご質問にお答えしています.